Should We Destroy The Euro?

High-debt countries do not outnumber low-debt countries at the ECB

This idea comes up again every few years from a different angle – we should break up the euro and we will live happily ever after, Europe’s woes will disappear. It has resurfaced as a comment by the respected Robin Brooks last week here.

I however find the argumentation weak and unpersuasive. Yes, we have many problems in Europe – low innovation and dynamism; few companies at the technological frontier; losing the geopolitical battles with the US and China; idle capital and savings; lack of top research institutions; low productivity and social systems under strain. Does destroying the euro help us with even one of those?

It is fashionable to criticize the ECB and its non-conventional instruments, especially the Transmission Protection Instrument, which indeed raises moral hazard issues. Criticizing policies is a normal part of democratic and academic debate. Pointing to individual channels through which ECB policies affect Member States differently and might lead to some countries “winning” and others “losing” is important so that we understand complex EU dynamics. This is what a recent paper by Hanno Lustig and co-authors does arguing QE represents a transfer of 11% of Germany’s GDP between 2014 -2023 to the periphery.

It is one thing to quantify and criticize separate EU policies, and another to say that in general some countries are losing and should therefore exit the euro (or the EU). Throughout the debt crisis 2010-2014, this was a powerful narrative in periphery countries, where people persuaded themselves the euro “destroyed” their economies. It was powerful in Italy, when the common saying was that Italy can just exit and return to exchange rate devaluations to make its economy competitive. Fabio Ghironi had a wonderful threat years ago arguing that with constant devaluations you are only going to artifically help your laggard, low productivity firms sustain their models a bit longer1. This is not how you get out of an innovation and productivity stagnation.

Funnily enough, at the same time the groundworks for the AfD were being laid in Germany with the very same arguments – here the euro was “destroying” the German economy! People tried to persuade us that Germany, the industrial engine of Europe between 2000 and 2020 was suffering from the EU construct. The voices from AfD wishing for German exit have gotten considerably milder since – and they have redirected themselves towards the real voter issue of the day which is migration.

It was however one thing to argue against the euro during the acute stress of the debt crisis and say that Germany was losing from “saving” periphery countries (it was not losing). It is another thing to argument for it today – when Germany has suffered from 3 years of recession and the euro could easily become an easy scapegoat for its current economic woes. Germany has gotten many things wrong in its economic policy, underinvesting in some areas, especially infrastructure, and relying too much on cheap energy imports (I say this with a heavy heart as I am quite fond of Germany and the Bulgarian economy is deeply intertwined with it). It is very convenient to say now – the euro is the problem, let’s exit!

This painfully reminds me of the not very smart “juste retoure” debate we also have on the EU budget. Every now and then the “net payers” in the EU budget (countries that pay each year more than they get each year out of the EU budget) complain about this and want a “juste retoure”. The long-term EU budget (the MFF) surely needs a lot of improvement – see my paper for the European Parliament here. Around 1/3 of the EU budget goes to “structural” funds – transfers to poorer regions to help them catch up to richer ones. A lot of this is infrastructure spending. These are money spent on roads, highways, airports. Bulgaria is one of the biggest “net recipients”, because it is a poor country starting from a low GDP level.

Who builds a lot of this infrastructure? Often it is a company from a “net payer” country – e.g. great companies like Strabag from Austria or Siemens from Germany. Here I am not saying this is bad at all or that Bulgaria is losing – quite the opposite, we receive funds, they are used, a competitive company builds some high quality thing for us and gets the revenues. But it will be unfair to say only “net beneficiaries” countries profit from this.

The idea that the euro is hurting Germany is not very different. Germany has enjoyed 20 years of very good economic growth and being at the center of the European economic engine2. The euro, giving Germany a safe haven status and a weaker currency (than it would otherwise have), can hardly have been a problem for that.

ECB decision-making is rigged in favour of high-debt countries

Most of all in Robin’s articles however I found this idea plainly wrong - “The basic problem is that high-debt countries substantially outnumber low-debt ones”. I just don’t get how he gets his arithmetic right here.

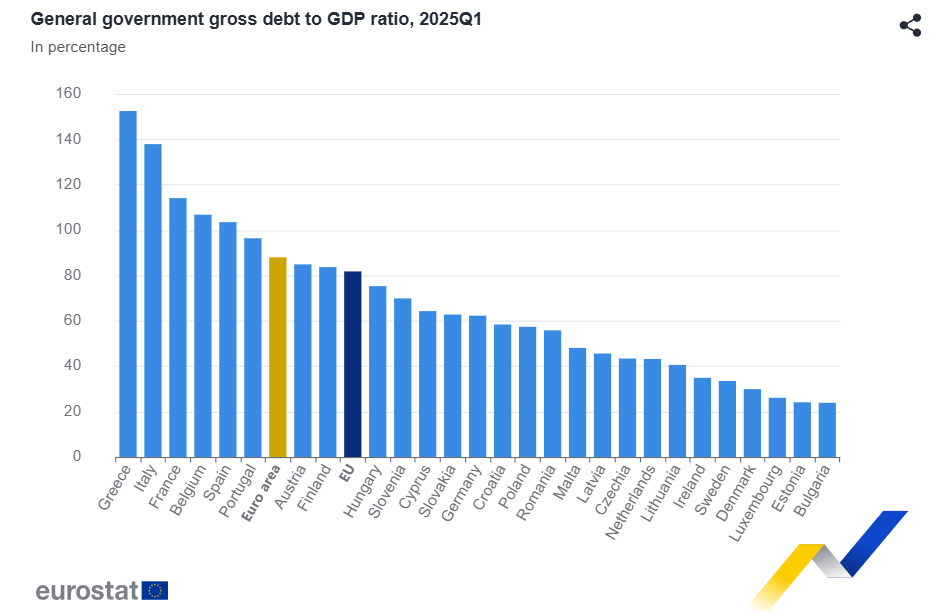

If you take the current euro EU (!) average debt to GDP ratio (see below), there are 6 countries with debt to GDP well above this average rate of 82% and 12 countries with debt rates below (Austria and Finland are fluctuating around the average)! Given that the governor of each Member State is present at each meeting of the ECB Governing Council and can state their opinion, there is no reason to say that the high-debt countries “outnumber” the low debt countries.

Let’s be more generous to Robin’s argument and assume that everybody who has higher debt-to-GDP than Germany is high debt and therefore dovish, self-serving and only takes decisions that profit high-debt countries. Even so, it is hard to even get to a parity - it does not make sense to count Slovenia and Cyprus, which have effectively the same debt to GDP ratio as Germany towards high-debt countries that conspire to hurt Germany (with the same debt to GDP). And Austria, which has a bit higher debt than Germany, until recently had the most hawkish of all governors. So at most you can add Finland and Slovenia to the camp of “easy on debt“. In this (generous) counting you still only get to 8 high-debt countries and 12 low-debt countries.

In case you want to count the Executive Board Member (which is not wrong), you would still get one French and Italian (very high debt countries), one German (let’s say mid-level debt, although that defeats the argument of Robin) and one Dutch and Irish (low debt countries). There is no way to make the count work.

Anyways, my point is that this counting exercise that high-debt countries outnumber and outvote low-debt ones is 1). wrong 2). stupid.

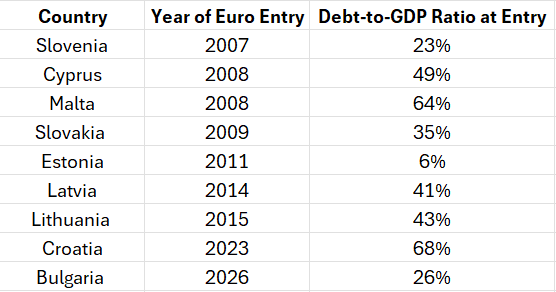

In fact, in the last 10 years ONLY low debt countries have joined the euro. Slovenia joined in 2007 at 23%; Cyprus, Malta and Slovakia - between around 40% and 60%. Then the three Baltics joined with debt-to-GDP levels below 45% - Estonia even had around 6% debt-to-GDP (which in macroeconomic terms is a bit ridiculous). Croatia joined at somewhat higher debt-to-GDP of around 70%, now down to 60%. Bulgaria will join also with a very low debt of around 25%3. If you look at this and are being cynical, one could argue that the game is actually rigged AGAINST the high-debt countries - in 20 years we had almost a doubling of euro area and all of the newcomers are with low debt levels (this is also embedded in the Maastricht rules).

Table 1: Debt-to-GDP Ratio when entering the euro - in the past 15 years, the euro area expanded with Member States with relatively low debt levels

Furthermore, all new joiners from Eastern Europe are also more likely to have higher inflation (because they are converging economies), so you would expect them to be more hawkish. So the Governing Council got 7 Member States of more hawkish countries, but somehow the game is still rigged in favour of high debt countries!

The final attempt to rescue the argument that the ECB is rigged to help high-debt countries (instead of just finding it sensible to do so in times of stress), is to argue that the new Member States do not matter because they are small economies. This is a deeply flawed argument, which was used also in Bulgaria to argue against our joining - I present the argument about it here. All you need to know is the following - at every Governing Council meeting, every governor of a central bank can speak and present his position. The Estonian and French one are represented in the same way. “Small“ countries can be represented quite strongly, when they want to be loud. Until recently, as mentioned, Austria had one of the most vocal hawkish Governing Council Members. Portugal and Austria have also had Executive Board Member. With Mario Centeno, who was Eurogroup president for years before that, Portugal has also been quite strongly represented while he was governor. Boris Vujcic from Croatia is the longest sitting governor in the euro area right now. These are just a few examples of why the counting of “small” and “big” countries is also faulty.

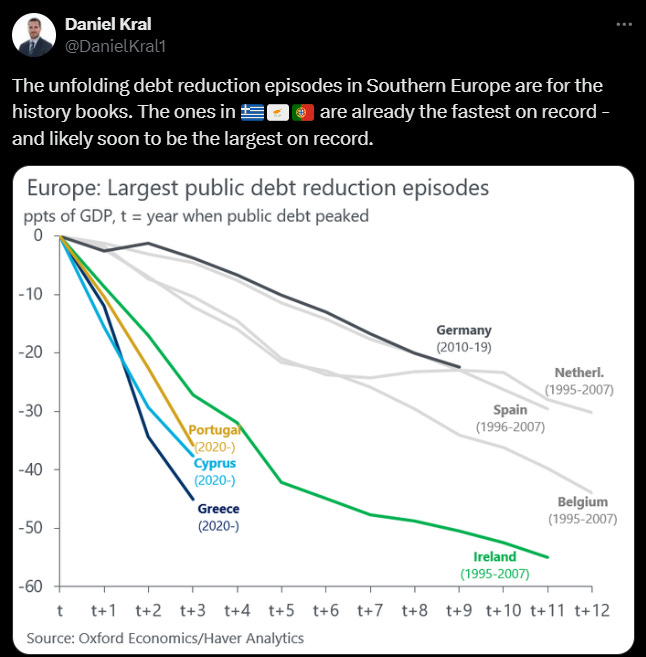

Finally, let us also remind ourselves the following - some of the so-called high-debt countries have undergone a record breaking period of REDUCING debt recently:

So instead of saying ECB voting is a conspiracy in favour of France, Spain and Italy, one should also consider another possibility if you believe that the ECB has been too lenient. Maybe the members of the Governing Council are not voting out of their selfish nationalist view – as Robin assumes for them, but have realised that the repercussions of too-selfish national positions also can hurt their own economies. This is why they have agreed to policies, which at first sight might look like favouring high-debt countries4. After all, we did try the opposite for years between 2010 and 2020. No TPI, no QE flexibility; every couple of weeks there was market stress and pressure (which should be good) on Italian bonds. Did that persuade or discipline the Italian state to behave in an according manner? I think it is hard to believe it has.

So the idea that breaking the euro will solve many of our current problems is far-fatched, but also dangerous5. It is a slippery slope that brings us to the same outcome as Brexit – a rich Northern-ish country is promised to have economic success by leaving because allegedly others take advantage of them. We know how that went.

In fact, any euro exit from a big country would most probably end the EU as a whole. It will antagonize relations, reduce trade and dampen growth with no clear benefits. We have so many problems - slow decision making; losing market share and competitiveness; high energy costs and much more. Countries at the core of the EU have profited immensely from it, especially the euro and the Single Market. So no, we should not destroy the euro. And at the same time, yes, when unsustainable, unproductive or dangerous policies are asked for (as Jordan Bardella did for France lately), of course we should also say a clear - Nein.

Source: Oliver Rakau’s Twitter

The Twitter search is not good enough anymore to help me find the thread.

This was partly driven by important labour market reforms and other structural policies, as well as competitive exports.

Achieved through years of underinvesting in infrastructure, healthcare and education.

Or, it could be that many of our macro models and the implications of them are neglecting moral hazard too much - or have other issues than make unconventional monetary policy, QE and forward guidance too much of a good thing. If these models and their conclusions are leading policy-makers decisions, this could be the explanation; unfortunately I am not sure whether macroeconomic research is as influential as I would like it to be.

The fact that some countries are underspending on Ukraine help is also not because they do not have fiscal space - it could be for any other reason. Maybe Spain, a country 4000 km away from Ukraine, just does not feel as threatened by the Russian aggression as the Baltics?

I agree with you that the demise of the euro would trigger a major financial and economic crisis in Europe. Some national currencies would crash, others would skyrocket. In which currency would creditors be paid? Intra-Euro Area trade would collapse, etc.. Your debunking of the argument that a majority of high-debt countries dominate the ECB is well done, as you quote the facts. The euro has already survived a severe crisis and overcome it by creating the missing mechanisms to avoid a repeat. To break the euro now would be madness. Let’s not lose time debating an issue that is not on the table. Just correcting wrong facts, as you did, is useful though.

Indeed @Atanas dismantling the euro would be throwing the baby out with the bathwater. It's not just the large one-off costs that would result from an inevitable euro-exit crisis. The net result for *all* European countries would be a *loss* of sovereignty as we'd get picked off one by one by the larger predatory powers - there's strength in numbers.

For core countries like Germany, it would be a disaster: exports would plummet at a time when the business model is under strain from Chinese competition. And if the problem is that countries should be able to default, surely the answer is reform - severing the nexus between banks and sovereigns - rather than destruction. Is reform slow? Sure. But I'd rather have that than the destructive, self-defeating unilateralism of the Trump administration, or Xi Jinping's unreformable rigidity which persists with a growth model that has reached geopolitical - never mind economic - limits.