Joining the euro in 2026 - does it even make sense?

Reflections on the pros and cons, fears and dangers of joining the euro for Bulgaria

I am resurrecting this blog after some years of silence. I will write mainly about Europe and economic policy. Sometimes we need to be diplomatic, but much more today we need to be blunt and clear on the challenges Europe is facing - otherwise we are at a real risk that our living standards, our economies and our common project becomes irrelevant on the world scene. We need to act in a manner, which projects strength; we need faster decision making (implementing the right policies); and we need better communication (to explain decisions taken). The blog is about this.

I decided to restart the blog with a long-ish threat on my views surrounding the upcoming euro adoption in Bulgaria – a topic I have been involved in for the past years as an economist, expert and as member of the caretaker governments in 2021/2022/2023, when I was part of the Coordination Council on euro adoption as Deputy Prime Minister. The comment is also based on a recent interview of ECB President Lagarde I watched on the Bulgarian National TV 2 weeks ago1. The topic was the entry of Bulgaria as the 21st member of the euro area on the 1st January 2026 with its implications. It was a good interview, but rather short, while the topic has been extremely divisive for Bulgarian society. So we need to strengthen up the argumentation, but also be honest about what the euro brings and what it does not.

The interview with President Lagarde started with the benefits that Bulgaria will receive from joining the euro area. I believe they outweigh the costs and risks associated and President Lagarde pointed some of them. However these may not be enough to persuade a sceptical population. Let us therefore cover again some of the main arguments for and against - interest rates, reduction of some costs, our position in the EU; as well as some of the often discussed dangers of joining.

Will interest rates go down?

What people in Bulgaria often want to hear is that interest rates for them (on mortgages & short-term loans) will definitely go down next year. But if we are honest, this is a broad question that cannot be answered definitely. Interest rates in a well-functioning modern economy are as much a price (the price of capital), as well as a tool of the central bank to steer inflation. So if the question is - will interest rates be lower next year than this year - we cannot decisively say that neither for the euro area nor for Bulgaria! Interest rates go up and down based on how inflation in the euro area is doing and how the ECB assesses the inflation path forward. So if something happens - the price of oil goes up, the price of energy goes up, another inflation shock occurs, the central bank (ECB) will increase interest rates! So we cannot promise you lower rates far off in the future (nor would that be advisable to have).

The relevant question is however - under the same circumstances in the euro area (and world) economy as today, would Bulgaria pay lower rates? One way to measure this is by the interest rate the Bulgarian government pays, but since this also varies with ECB interest rates, economists measure it as a spread (the difference) to another economy. As the biggest and most central economy, we always measure this vis-a-vis Germany. The spread that comes out is a measure of how much more “risky” your debt is in comparison to the safest EU government debt - the one of Germany. We already saw improvement on that front (and all rating agencies have upped our credit ratings in recent years) - the Bulgarian spread to German government debt has decreased throughout 2025 (from an average of 1.6 pp in 2024 to an average of 1.3 in 2025) as the euro prospects have strengthened and the decision was finalised. And this happened at a time when our government deficit has worsened throughout 2025 (which should have pushed in the opposite direction).

The positive effects on interest rates for the Bulgarian government are therefore clear. This might seem small, but a 0.5 percentage points decrease in the interest rate on government debt results in savings of tens of millions for the Bulgarian government. This could be used for something more productive than repaying debt to international investment banks as we do now.

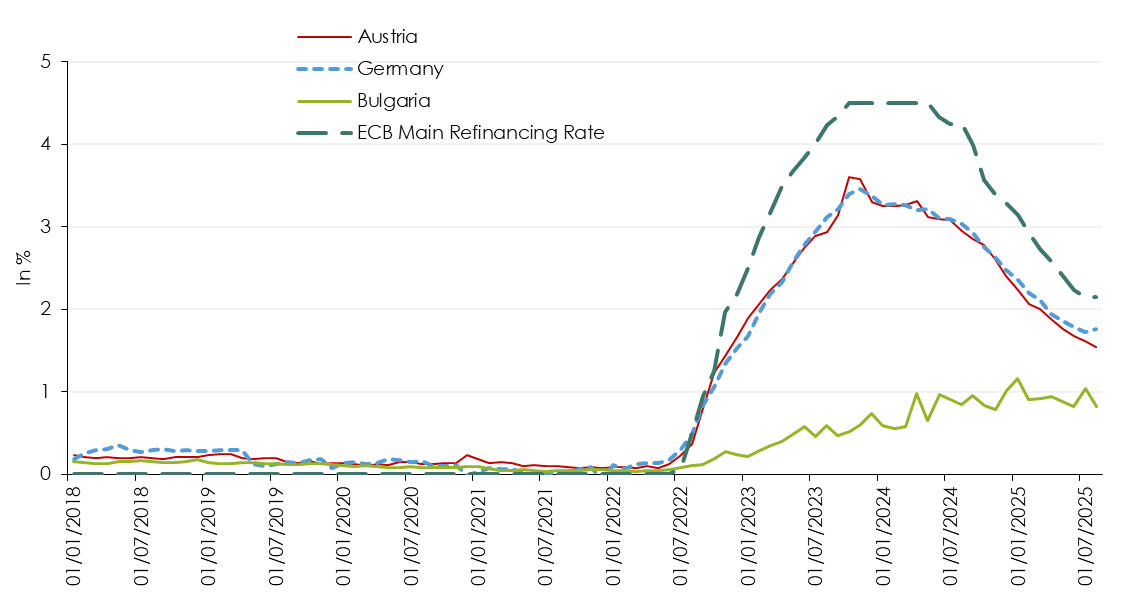

Will that lower cost of debt for the government be transmitted to the citizens and businesses of Bulgaria? In most countries in the euro area government bond yields and interest rates for firms and citizens are well correlated. This is however not the case in Bulgaria. The next two graphs visualise this - and are a signal of a not so-well functioning market process in the financial sector - in our case due to extremely high liquidity (deposits by households) and weak competition in the banking sector. Lack of competition for customers, as banks are flush with deposits, leads to pictures like this - the average interest rates on deposits in Bulgaria have barely moved for years and are still below 1%, even though they increased markedly in the euro area, Germany & Austria since the ECB increased interest rates 2 years ago:

Figure 1: Deposit rates of households up to 1 year (total) and ECB Interest Rate (Main Refinancing Rate). Source: ECB, Bulgaria National Bank, Macrobond.

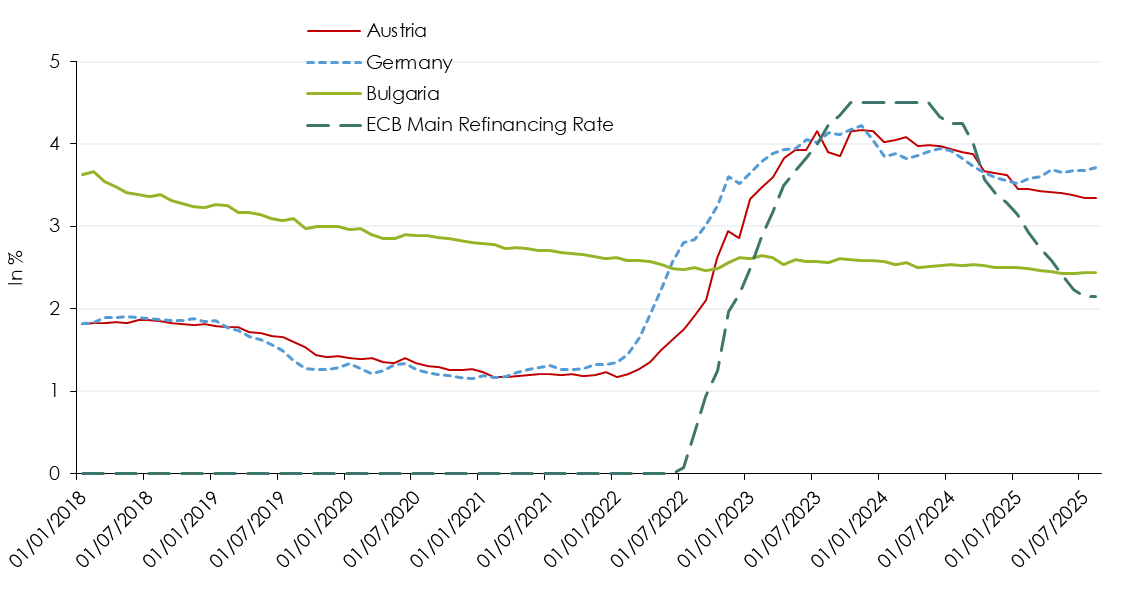

Similarly on the credit side, interest rates for house purchases have also barely moved in recent years, while the ones in Germany and Austria were for a prolonged period close to 1.0% (so households benefited from low rates there) and then increased to above 3% during the ECB interest rate hiking cycle.

Figure 2: Interest Rates for House Purchase and ECB Main Interest Rate (Main Refinancing Rate). Source: ECB, Bulgaria National Bank, Macrobond.

All in all, these are not good signs for the transmission of ECB interest rates to the Bulgarian financial sector, but these have very little to do with the ECB and the euro as a whole - as you see, this was the case pretty much throughout the last 7 years and it has to do mostly with national conditions and lack of competition.

President Lagarde then spoke about the further benefits of the euro introduction - the lack of exchange rate volatility, the savings from conversion and transaction costs and our inclusion in the ECB Governing Council decisions.

“Bulgarians will profit from lack of exchange rate volatility and lower transaction costs.” This is true, although the first part is not so relevant for us, as exchange rate volatility has been eliminated already for 25 years since Bulgaria adopted the currency board in 1999. By adopting the currency board and pegging the lev to the euro, we already trusted the euro and the ECB - the decision to have a currency board is a decision to say - I do not trust my central bank could and would do what is necessary to keep inflation under control - so I will give the power of monetary policy to somebody else, who could do it better. This is what we did in 1999 and it worked very well - so much that the currency board is one of the most popular decisions in Bulgaria2. But we need to remind ourselves that the shadow risk of re-denomination always crawls behind a currency board, which could be eliminated with a simple decision by Parliament - and if markets decide so, you can lose it very fast.

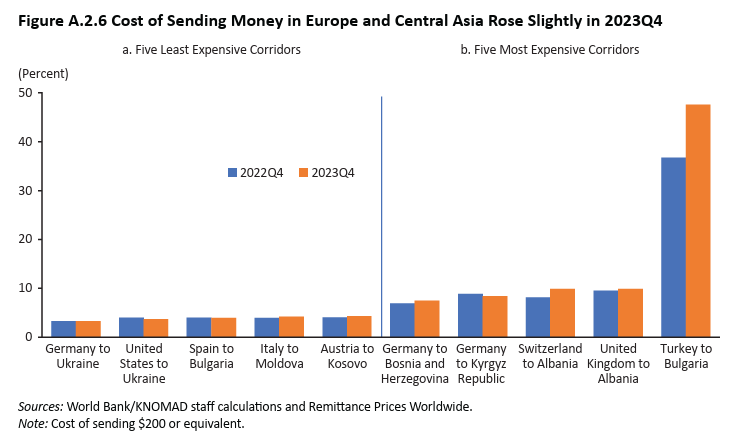

President Lagarde also mentions that we will save from transaction and conversion costs. This does not get talked enough, as people think the savings will be very small. Bulgaria receives very high remittances from Bulgarians abroad each year - the World Bank Migration and Development Brief 40 reports them at 2.5 billion USD. The remittances are so high in Eastern Europe that Branko Milanovic some years ago noted that they are often higher than the total Foreign Direct Investments in these countries! It is hard to estimate how much of this is from the euro area and how much from the rest of the world (mostly US, UK, Türkiye), so let us split it in half. What is the conversion cost paid on them?

If you send money from Austria to your euro bank account in Bulgaria, indeed there is almost no cost (but you still have to convert the money into lev to pay with it). If you send money from an euro account in Europe to a Bulgarian account in lev though or you take euro cash with you and exchange it at a currency exchange in Bulgaria, the transaction and conversion fees raise to about 0.3% - 0.5%. In that case, Bulgarian citizens will be saving an average of 5.5 million euro per year (~11 million leva) when these costs are eliminated. This is not much, although for a country constantly underinvesting in education and healthcare, just throwing 11 million leva each year for useless conversion is already something.

But the same World Bank Report3 reports that even a transfer of 200 Euro from Spain to Bulgaria actually has on average an exchange cost of around 3% - 4%. This raises the estimate of the conversion costs - if we assume half of the euro remittances are conversed under these very high costs; then annually Bulgarians will save instead around 21 million euro (~ 42 million leva). And this is only the saving from remittances - the money Bulgarians send from abroad to Bulgaria. When we also add the money Bulgarians spent abroad (through travelling or ordering something directly in euro - Bulgarian spent close to 1 bn euro abroad in 2024, while the BNB BOP Travel Debit statistics reports around 3 bn euro per year), the savings most probably double or triple up! And this is only the savings of citizens - without considering the savings of private businesses, which are already very intertwined in the euro area economy (and which for years have pushed for euro adoption).

Figure 3: Costs of Sending Money from the World Bank Migration and Development Brief 40. Costs of sending from Spain to Bulgaria are considerable at around 3%-4%.

“We decide and you obey”

Yes, better credit ratings, lower government debt costs and the savings of millions of euro for citizens and firms are nice, but what does the euro really give us? Well, it gives us representation. And in the times we live, where nationalist and sovereignist feelings are dominating politics, this is important. We should not neglect the sense of national pride and the ability of the sovereign to control its own destiny, as we see it is a winning formula in elections across the advanced world lately.

Much of the opposition in Bulgaria against the euro today is based on the view that Bulgaria will LOSE sovereignty by joining the euro. This is wrong. Currently, because of our sovereign decision to create the currency board in 1999, the ECB has been deciding monetary policy for Bulgaria for 25 years and we just obeyed this decision. That is right, every 6 weeks, the Governing Council of the ECB gathers and decides what will be the interest rates in the euro area; a couple of weeks after that, the Bulgarian National Bank does the same step to keep up the currency board.

What President Lagarde therefore should say is that right now the status-quo is that the ECB decides and we just obey. By joining the euro area, Bulgaria will now be part of this decision-making process. Her response at the September GC Meeting press-conference was to the point: “Bulgaria now has a voice and a vote. Each euro area member around the (ECB) table has a voice which is regarded, considered and respected exactly as the other ones, no matter how big or small”.

And in fact the way that the ECB works we will be overly represented. Some media outlets reported in the summer that Bulgaria will not have much influence in the ECB Governing Council because it is a small country - but this is completely up to us and our governor and central bank. Opponents of joining the euro often mention the so-called voting rotation that was introduced when the euro area got bigger some years ago. Yet they do not tell you the full truth - the ECB Governing Council does not vote on most occasions. Unlike the Bank of England and the Fed, where you have votes for and against any policy measures are reported - the ECB takes decisions mostly by consensus. The Governing Councils meets for a long, two-day discussion every 6 weeks. All Governing Council members are there and participate in the discussion, the voting share does not restrict them. The ECB has only seldomly in its 20 years history done an official vote count on a policy measure. So in fact, instead of having ZERO influence, now we will sit on the table and can get the influence we want to have (based on how “loud“ our position is). Being a smaller country does not restrict you to have a “weaker“ voice - the former governor of the Austrian National Bank Robert Holzmann had an extremely loud position in the Governing Council, although Austria accounts for around 2% of the GDP of the euro area. World leading media were reporting on his views and positions constantly - would that be possible if he was deciding only the monetary policy for a mid-sized European economy like Austria?4

So to summarize - for 25 years we have had no control on monetary policy, for 5 years we have also outsourced part of our banking supervision5. Now we get to be represented at the main decision-making body of the ECB. So instead of being angry to be part of the decision-making body of the second most important currency in the world, the nationalist right should focus on having good candidates to be in charge of the central bank if they ever take power6. Here by the way President Trump has consistently performed well even though he criticizes the Fed harshly - his first pick for Federal Reserve Chair Jay Powell has been stellar in the past 9 years and the favourites to take from him next year - Chris Waller, Kevin Hassett and Kevin Warsh are all very competent people with good reputation.

But the euro is doomed

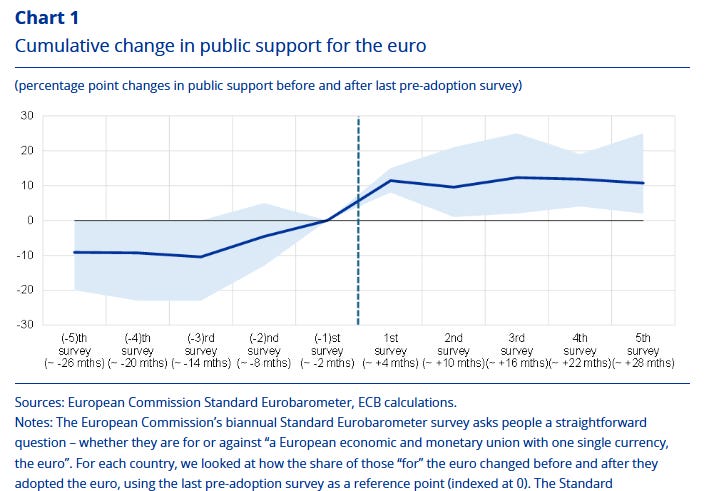

The above arguments are all well and fine, but of course with any big transition process, the process of euro adoption leads people to concerns about the dangers, risks and costs. President Lagarde mentions rightly and honestly that a change is always a cause of concern. These concerns seem to be transitory - the ECB just came out with a blog post showing that after the adoption finally happens, the popularity of the euro increased on average by 10 basis points in Member States (and the euro is at a record high favourability in 2025 according to Eurobarometer).

Source: ECB Blog: “Love at second sight: support for the euro before and after adoption”

But until this happens, it is an open discussion of opinions whether the euro will “save us” or “destroy us”. The debate in Bulgaria has been unnecessarily aggressive and heated in the last few years, driven by common divisions of our society related to geopolitics. I think that was a lot of wasted time and effort on both sides. Now that the decision has already been taken - and it is always a political decision first and foremost, we can be honest about the path forward. There are significant positives explained above. But there are also concerns.

There is a meta discussion in Bulgaria that focuses on the long-term sustainability of the European Monetary Union (euro area). It has lead doomsayers to conclude that the euro will crash next year (they have been repeating this now for many years). I do not subscribe to this view and do not see the euro area as unsustainable. It has survived the Global Financial Crisis, the euro area debt crisis, the pandemic and the energy shock. This required a lot of ad-hoc measures, because indeed the EMU is not yet complete (or as we say - it is not an optimal or a complete monetary union yet). But it did survive - like the infamous bumblebee analogy of Draghi, it manages to find ways to fly even amidst extreme shocks in its Member States. The euro has evolved further with each crisis. As with many issues of monetary and financial nature, as long as there is trust and confidence in the project, the necessary architecture and policy refinements can be done to sustain it. I do not see fundamentals right now that point to a clearly unsustainable path for the euro.

But there are indeed real issues in the euro area, which raise concern. 7 Developments such as the budgetary woes of France are worrying to say the least. Recent weeks raise some troubling questions for the future of the EMU if one of its core members does not find political consensus to implement well needed reforms and reign in its deficits. Indeed the ECB TPI ameliorates the pressure on France to act to correct its huge budgetary imbalances8. So something needs to be done on this front and soon. And on top of that, there is the real possibility - which I consider almost a certainty - that either Front National or AfD will sooner or later win national elections in France or Germany, with major implications for the euro, depending on what they decide to do in power. We should therefore be open about the problems the euro area has, without being apocalyptic or chastising people who point to them.

Finally, I want to finish with something positive. Bulgaria indeed is lucky to be joining at the right time. There was some push in previous years to join as fast as possible - and pressure on governments to negotiate with the European Commission as fast an entry as possible. Indeed, the rules were a bit unfair and kept us out longer than expected - because during a high inflation episode, it was extremely difficult for a converging economy like ours to fulfill the inflation criterion. I have had numerous meetings with European Commission and IMF officials pointing to them this imbalance.

But in fact, ex-post I consider it was very good that they did not let us in earlier - when inflation was higher in e.g. beginning of 2024 or 2025. Indeed it is the worst possible time to enter when inflation is very high. Our friends from Croatia, who were very well prepared for the entry, had this bad luck to enter the euro at a time of record high inflation. Whether just or unjust, many people now blame the higher inflation on the euro - and it might partly be true, as in times of high inflation the inevitable rounding-up that sellers do ends up being even higher than in times of low inflation. Bulgaria therefore is lucky to be joining at a time where inflation is relatively calm at around 3%-4%.

And we are entering at a decisive point for geopolitics - when the world seems to be changing everyday at a rapid pace. The euro is a geopolitical decision for us to integrate further in the processes of the EU. It has some positive implications in saving us money for conversion and exchange, for improving our credit rating and therefore making our debt cheaper, and for strengthening our representation and our ability to be part of EU decisions. My believe and hope is that by joining the euro, the second most important currency in the world, we will be able to participate, decide and steer it into the right direction so it can serve citizens of our Union in the best way possible. It is not a panacea or a growth-enhancing miracle. It will not make you rich on its own, you do not even need it to be successful - look at Poland. It is only one step, a milestone that helps you with more security and certainty, better credit rating, no shadow risk of doing something crazy, some costs spared, a seat at the table. And to be successful you need to built on this small step with growth-enhancing policies, with reforms that ensure the rule of law (instead of backsliding into lawlessness) and with investing in your talents, technology and well-working institutions. Without all this, the euro will not lead you there where you want to be.

There were more interviews this week and a high-profile conference this week in Sofia that I could not attend so not commenting on those.

The period before the currency board was a period of nauseating inflation of more than 500%.

Figure A2.6. - Cost of Sending Money in Europe and Central Asia Rose Slightly in 2023Q4

Furthermore, Bulgaria also joined the Banking Union in 2019 as a preparatory step for the euro. We were the first country to be asked (politely) to join the Banking Union BEFORE euro accession, so that the ECB could oversee and do an asset quality review of our banking system - something that could also be seen as losing sovereignty and supervisory power - yet so far I only see positive repercussions on the stability and credibility of our banking system from this move.

See footnote 3 above.

A suitable extra-conservative candidate should at the least be very competent in terms of opposition to greening the ECB balance sheet and should focus on a narrow mandate and a close scrutiny to the TPI.

The criticisms made by many and explicitly well in the recent book by Cochrane, Garicano and Masuch, make a lot of sense. I respect the authors, even if I do not share a lot of their conclusions.

Although I do not remember fondly the time before the pandemic, where we had the opposite case - no interventions by the ECB for individual countries, which meant that each miniature political development in Italy could sent markets into turmoil. This did not make Italy rethink its budgets back then.