Saving the Euro, one Eurogroup meeting at a time

"Either the EU shows itself willing to provide substantial help to member states in trouble or it has no reason to exist"

The past month has been a breath-taking moment of modern history. It is surreal to think that some 30 days ago, in much of the Western world, we were preoccupied with Super Tuesday or our weekly football games. So much has changed since then and the almost complete lockdown of parts of the world economy has unfortunately resurrected many old wounds. In Europe, the never-ending fears about a Eurozone break-up have returned with a vengeance and were embarrassingly acute at the Eurogroup and the European Council meetings in the past weeks, like a married couple fight broadcasted on national television.

The coming months will be a challenge to the Euro area, so all eyes are on the Eurogroup meeting today, 7th April, where Eurozone finance ministers need to find a more constructive way for solving their differences - fastly and decisively, without too much extend and pretend on the issues facing the Eurozone going forward. In the recent IGM Economic Experts poll, as well as more widely, there seems to be a consensus that a Pan-European fiscal response will be needed (agreed by 90 % of the economists asked in the European IGM Economics Experts Poll) to counteract the consequences of the crisis. Some countries have already launched massive stimulus programmes, but for others, such as Italy or Spain, this might be prohibitively expensive if yields start raising again. Looking at the market reactions from the decisive third week of March already gave us some hints to that.

Alexander Hamilton at the Battle of Trenton, December 26, 1776; Note: Why is Alexander Hamilton important for the Euro area in 2020? This deserves a separate blog post.

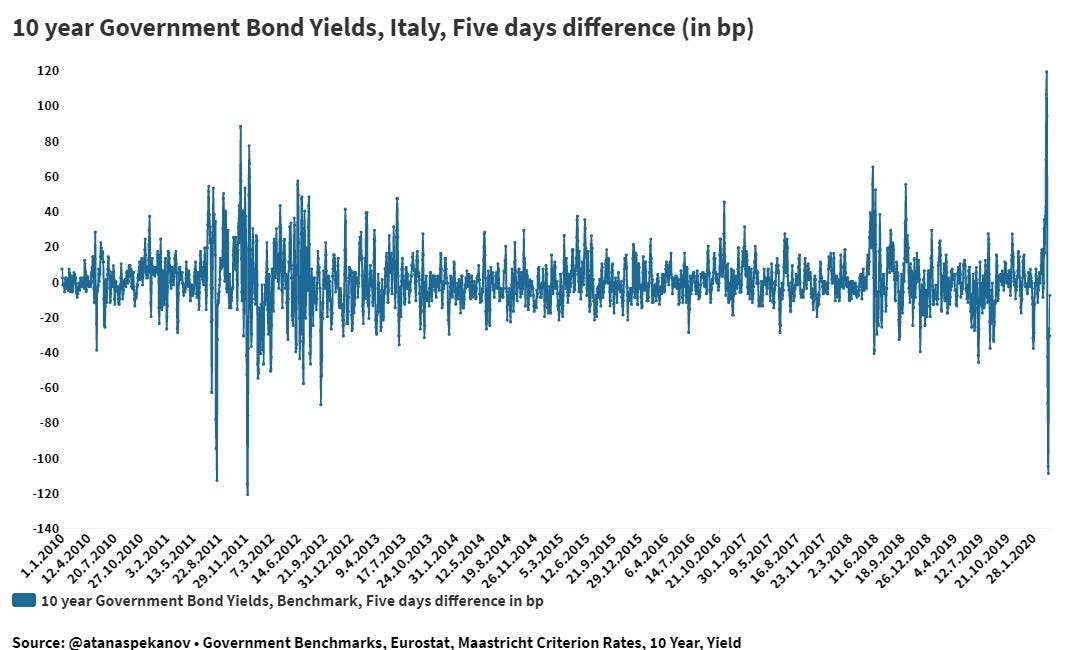

Should we be expecting a real return of the Eurozone crisis? On one hand, if the idea that the economy is just frozen in a “medically induced coma” for the time being is correct, and given that banks are much better capitalized today than 10 years ago, we should be hopeful that the first phase of the current shock is mostly a shock to the real economy, without direct repercussions in terms of banks and financial stability. However, government bond markets showed a different story in March. Government bond yields in Italy surged massively – taking the 5 days difference in 10 Year government bond yields, one can see in March the biggest weekly increase for Italy in the past decade (Figure 1 below). Between 12 March 2020 and 18 March 2020, Italian government bond yields rose 119 basis points. This is the biggest 5 days increase in Italian government bond yields, dwarfing the previous high of 9. November 2011 (88 basis points), the day after Silvio Berlusconi resigned as Prime Minister of Italy. It also leaves far behind the June 2012 period, when worries about the Euro area periphery pushed yields higher before the Spanish rescue package (57 basis points increase for Italy); the 65 basis points increase due to budget uncertainties of the new government in the end of May 2018 and the 0.64 increase in the end of October 2008, at the onset of the Great Recession in Europe. The March 2020 increase thus beat some of the most worrying days of the Euro area crisis for Italy. The same however did not hold for the rest of the Euro periphery as a whole – only Spain and France had similar significant increases.

Figure 1: 5-Days Changes on 10 Year Government Bond Yields for Italy; Note: The third week of March recorded the highest 5 day surge in yields (119 basis points), even higher than during the Euro area crisis (followed by the biggest decline, after the announcement of the ECB PEPP programme)

Yes, the ECB has helped and intervened decisively on the 18th of March, which has successfully pushed spreads down and gave national governments air to breathe and concentrate on the health situation, therefore ensuring the monetary policy transmission mechanism is safe and thus following its mandate. The PEPP programme has also introduced most welcome flexibility to enable the ECB to buy as much of one countries bonds as needed. However the overall programme is limited to a maximum extent of € 1.1 trillion (unlike its unlimited Federal Reserve big brother). Would this be enough?

There are huge uncertainties around the next months. What if, the frightening prospect materializes that the Hammer and Dance strategy does not work and that we cannot sustain a “controlled normalization”? Some preliminary evidence from Singapore and South Korea offers first example that opening up the economy prematurely can induce a second wave of contamination. Is the PEPP then going to be enough to limit new pressures on financial markets following such a shock, e.g. a prolonged or a second lockdown? Can the ECB PEPP programme be extended further? Is that even desirable? It was said over and over again, the ECB cannot be the only game in town. The answer has to come through a coordinated fiscal response.

The Eurogroup today stands in the middle of a decision how to design such a response – between the now vocal support in favour of a one-off “Coronabond” financial instrument, backed by the 9 country leaders that signed the plea to the European Council two weeks ago in favour of such a new instrument, and the support by other countries for a traditional and arguably easier to implement approach of giving credit lines from the European Stability Mechanism. The ESM option of providing a credit line to national governments, that can tap into and thus secure relatively cheap financing, seems like the easier way out and is already administratively available. A main downside is the fear that the € 410 bn. capital of the ESM might not provide enough fiscal help for countries of the size of Italy or Spain - in comparison to the now discussed € 1 tn. “Coronabond” one-off issuance. The funds from the Coronabond can also be distributed according to needs and thus ensure that proportionally more be given to the most struck countries. The size of the ESM can however be expanded. The real fear behind requesting money from the ESM in Italy comes from the “stigma” that comes with being dubbed a “programme country” and the conditionalities that might be attached to implement structural reforms – many of which have been seen during the Euro area crisis as excessively harsh on ESM programme countries. German Ministers Olaf Scholz and Heiko Maas have pledged however in a joint article yesterday that there should be no strict conditionalities in providing help for such an unprecedented crisis. It is ironic that periphery countries have always feared the stigma of being helped by the ESM – of signalling that you might be in financial trouble, thus raising uncertainty about your fiscal health, but the stigma today also goes the other way around, as the ESM is also stigmatized, even if it would agree to lend on relatively mild conditions - as the teacher who was too strict and nobody wants to take their course anymore. While the ESM is seen as toxic in Italy, on the other end, many have deemed Coronabonds “dead on arrival” – either because of the time it would take to introduce them, due to the legal challenges of doing so or due to fears of debt mutualisation. As a number of pieces have however tried to explain – a one-off debt instrument could be designed to be legally workable and to avoid future debt mutualisation or transfers after the current crisis. In one of the most practical suggestions Christian Odendahl, Lucas Guttenberg and Sebastian Grund propose to share the fiscal burden of the crisis through a “Pandemic Solidarity Instrument for the EU” and show how this could work under EU law.

It was a good first step by the European Commission last week to present a small form of risk sharing through its new SURE programme, providing credits for Member States to pay for their short-time work programmes. The € 100 bn package for SURE will not be enough however. To expand this, the German Finance Minister has proposed a three-pronged strategy yesterday – liquidity support for firms through the EIB, funding for employment programmes via the SURE scheme and an ESM credit line. A number of the leading experts on Euro area reform have pointed that „The need for a strong, quick and significant European initiative is beyond doubt” and that it “calls for a multi-instrument approach that would jointly achieve three objectives: sharing the cost of the COVID crisis, helping member states to borrow at very long maturities and low interest rates, and relaunching the EU after the crisis”. Would that be enough? Many believe that the situation will inevitably require some one-off transfers, not only credits.

So both sides of this discussion are currently in a trench war, which has to be solved as soon as possible with some middle of the road agreement. The risks of not showing solidarity with the countries in need today are very profound and risk the future of the EU project as a whole. Jean Monnet, said in 1976 that

“Europe will be forged in crises, and will be the sum of the solutions adopted for those crises.”

These words ring true today. While Monnet was right, that Europe is forged in crises, it is being kept alive one European Council and Eurogroup meeting at a time. This is a dangerous balancing act and policymakers and governments should realize that wrong or unfair decisions today leave wounds in some country capitals for the future. They should start finding their common ground today. As Luigi Zingales wrote yesterday:

“Here we make Europe or Europe will die… Either the EU shows itself willing to provide substantial help to member states in trouble or it has no reason to exist”.